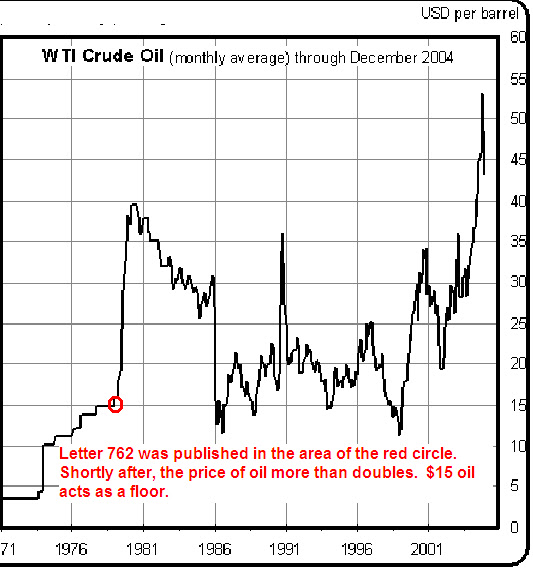

Letter 762 was published on August 1, 1979. At the time, the Dow Jones Industrial Average was indicated at 839.76. There were a couple of items that stood out as I read this newsletter.

Richard Russell said:

“As a matter of fact with Libya’s recent 10% cut in oil shipments and Algeria’s just announced 20% cut, I suspect that there’s an oil (and gas) glut building up now! The world is learning to cut back on fuel use—and fast, and this could turn out to be the shocker of 1979-1980.” Page 2.

In fact, it wasn’t long before oil prices reflected the glut that Richard Russell spoke of. Under normal circumstances, it would be difficult to see beyond the present crisis and think that it will end at some point. It seems that Russell was cognizant of the prospect, as remote as it seemed at the time. Unfortunately, as indicated in the chart below, $15 oil would become a base, or floor, instead of a ceiling.

One item that has been a longstanding issue with Richard Russell is reflected in the next quote.

Russell said:

“Last week I was asked this question: ‘Russell, if you could change any part of your stock approach over the past year, what would have done?’ My answer was, ‘There are many subscribers who are willing to speculate, and I think I have been too conservative and too stubborn on this issue. The change I would have made is that I would have offered speculative choices for those willing to assume the risk of buying in a market that is not over-sold and not in an ideal buying area.’” Page 2.

In addition to the previous remark by Richard Russell, he also said:

“I want to add that I personally am buying no shares here. I prefer to wait for the ‘ideal buying situation.’” Page 2.

The two remarks above have been the biggest challenge to Russell’s ability to adhere to Dow Theory or even his Primary Trend Index which was created to avoid potential market manipulation. Russell is infinitely waiting for the “ideal buying situation” while ignore individual values along the way.

Russell points out a fact that every investor should have ingrained in their mind before committing a single dollar to the stock market or any other potential investment opportunity. Russell said:

“Every investment must ultimately be valued on its return. In the stock market that means dividends. Ultimately, dividends must be paid if a stock is to be worth anything.” Page 4.

I thought that the following remark was profound.

“Now here’s an interesting aside on inflation. One of the reasons it’s so insidious is that as soon as a man starts protecting himself against it, as soon as he buys a house or a load of gold coins or a painting or a stamp collection-that man wants his inflation hedge to go up. He becomes (deep in his heart) an inflationist. Take housing: the value of total housing in this nation is $2.2 trillion (two thirds of these houses have mortgages). The last thing these home-owners want is a declining market. They are secretly in favor of rising prices and inflation.” Page 4.

Russell’s comment is right on target when it comes to the attitude of most people. It seems that everybody is an inflationist. There are few market participants or commentators who express the view that they hope their long position will decline in value. The NLO team happens to be among the few who, after going long a stock, are eagerly anticipating a decline in price. Shameless self-promotion aside, Russell’s commentary on the closet inflationists is truly profound.

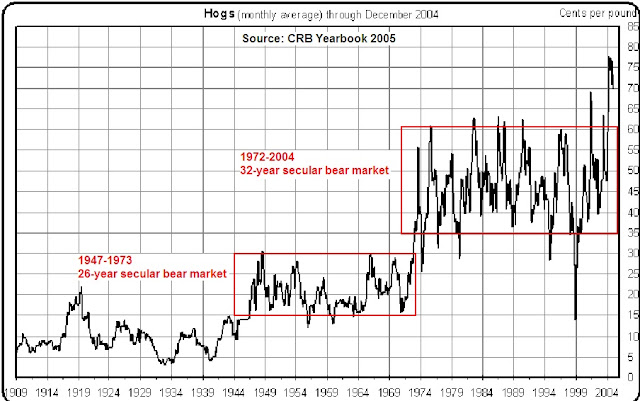

Russell points out that if you’re in commodities but not in precious metal then you could be losing your shirt. Russell says:

“Commodity traders have had one of their roughest seasons in years. If you weren’t in the metals, you probably ‘got killed.’ For instance, the October cattle contract is now down from 74.45 to 61, a drop of almost 18%. One trader told me that ‘it looks like the country is vegetarian.’ Live hogs are much worse, with the October contract dropping from 51 to 32 a drop of 37%. On piggies I was told that they act like ‘the whole world is going Jewish!’” Page 5.

This counters the belief that during inflationary periods, all commodities do well or go up in value. It should be noted that the declines that were mentioned by Russell could have been the equivalent of a temporary pullback or secondary reaction. Interestingly, monthly hog prices traded in a wide range from 1972 to 2004 as indicated in the chart below. Suffice to say, anyone involved in commodity trading should be willing to accept even greater losses than the 50% that we expect for long positions in stocks before seeing any gains.

On the topic of interest rates Russell says the following:

“To the casual observer, it looked like a world embroiled in an interest rate war. And the fact is that rising inflation is being fought all over Europe and Japan- via an interest rate squeeze. The US is a frightened and reluctant follower.

“A few weeks ago Germany raised her bank rate. At the same time Britain boosted her borrowing rate a whopping 2%. Last week the US raised its discount rate an insufficient .5% to a record 10%. Canada immediately followed with a boost to 11.75% in her bank discount rate. The Japan jumped her lending fee to institutions a full 1%.” Page 5.

My thoughts on this passage are that it seems fascinating that the US wasn’t taking the lead in interest rate policy. Especially in comparison to the countries that were mention. It may have been a purposeful attempt to adjust rates when it was absolutely necessary. Could you imagine interest rates jumping 2% at a time?

Russell indicated that as the world’s leading power, the U.S. with its excessive printing of dollars cannot continue unabated. Russell said that foreign holders of dollars would become anxious and “move towards the exits.”

Russell mentions the Gold/Stock ratio; which divides the price of gold by the value of the NYSE Composite. Of the rising trend of the ratio, indicating strength in the price of gold, Russell says:

“Day after day the ratio climbs higher, and it is clear to me that shortly, SOMETHING IS GOING TO GIVE.” Page 5.

With hindsight being 20/20, my thought is that what “gives” in this situation is high inflation unless Russell was proposing that all governments are going the way of hyperinflation. My observation is that what tends to break, when two normally divergent indicators are going in the same direction, is the one that appears to be the “strongest.” In this case the stronger component of the Gold/Stock ratio was gold which had been in a multi-year rising trend while the NYSE had been in a wide trading range for an extended period of time.

I do have concerns about the sensibility of a gold/stock indicator since I have presented the view that gold and stocks usually follow each other rather than move counter to each other. For the most part, we have seen gold lag on declines and lead on rises in the stock market. One thing I’m certain of, if the price of gold rises then the stock market isn’t far behind. There may be an occasional divergence but the overall picture is that gold and stocks generally move in unison.

More: