Flash Crash Follies is a running tally of stocks that get ensnared by

regulations as an outgrowth of the May 6, 2010 "flash crash." While the explosive crash of stocks (either up or down) on the NYSE is a symptom to a bigger problem, we want to chronicle what was never reported to have happened before May 6, 2010. Action packed moves in the price of stocks that will bring pleasure, pain and finally resignation at the state of the free market as we know it.

We've added commentary from the mouthpiece of the NYSE or NASDAQ to explain away "erroneous" trades or canceled orders. Before long we're going to hear politicians getting into the fray on specific "erroneous" trades. What will this devolve into nobody knows for sure. However, we're willing to bet that in due time, the treatment of the symptom will become a distinct problem of its own.

"...the folly of human laws too often encumbers its operations." Adam Smith

September 28, 2010 (date contains Bloomberg screen shots from third party source)Apple (AAPL), Research In Motion (RIMM), IBM (IBM), Dell (DELL), General Electric (GE), Oracle (ORCL), Microsoft (MSFT), Hewlett-Packard (HPQ)

Stocks of the above noted companies took a dive at the same time on September 28, 2010. The exchanges didn't provide commentary on the actions taken as a result of the instantaneous decline and rise in value. many have attributed specific declines to "newsworthy" issues related to the specific companies. However, no one has stepped forward to explain the statistical anomally of so many companies experiencing the same issue at exactly the same time.

July 29, 2010 (date contains article link from third party source)

Cisco Corp. (CSCO)

At 10:41am EST, Cisco (CSCO) shares spiked by 11% due to an order imbalanced triggered by 100 shares. CSCO rose from $23.37 to $26 which triggered circuit breakers prompting Jamie Selway, managing director at broker White Cap Trading LLC in New York, “We’re stopping trading in incomparably liquid products because of dumb mistakes...” In this instance, the NYSE-owned AMEX which handles very few trades in CSCO could not fulfill orders placed on their exchange even through there were plenty of shares being trades on alternative exchanges. Ultimately, CSCO was trading with the liquidity of a penny stock. Soon enough, firms with intimate knowledge of where they place their trade can play the illiquidity to their advantage. The AMEX and other small exchanges will be under attack.

July 23, 2010 (date contains article link from third party source)

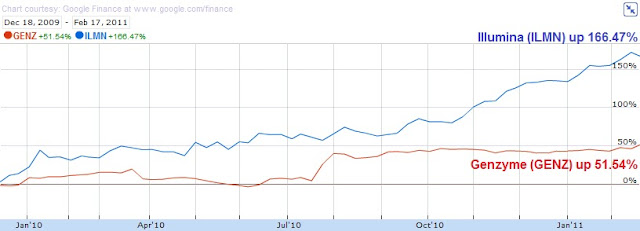

Genzyme Corp. (GENZ)

At 1:18pm EST and 1:25pm EST, Genzyme Corp. (GENZ) triggered circuit breakers when the stock attempted to rise by more than 10% on two separate occasions within the same day due to rumors about a takeover. Nasdaq OMX spokesman Robert Madden gave no justification for the halt in trading. However, traders and money managers expressed the sentiment that “at some point, you need to let efficient market theory rule how stocks trade.” In this case, Genzyme wasn't allowed to rise as much as speculators were willing to bid the price up.

July 6, 2010 (date contains article link from third party source)

Anadarko Petroleum (APC)

At 10:56am EDT to 11:01am EDT, Anadarko shares trade from $39.14 to $99,999.99. “‘We are still learning from the experience,’ he [Ray Pellechia] said.”

June 29, 2010 (date contains article link from third party source)

Citigroup (C)

At 1:03pm EDT, Citigroup shares trade from $3.80 to $3.3174 or down 12.7%. “The erroneous trade was subsequently canceled, NYSE spokesman Ray Pellechia said.”

June 16, 2010 (date contains article link from third party source)

Washington Post (WPO)

At 3:07pm EDT Washington Post stock trades from $450 to $919 or up 104%. All trades were cancelled. “‘What happened today was not due to a substantive, true move in the stock. It was simply an error,’ NYSE spokesman Ray Pellechia said.”