A research request is a response to our reader's question regarding Applied Materials: "Do you like AMAT? They just raised their dividend and seem close to an average low." Our team wrote a brief response with the article titled "Applied Material and the Chip Sector Should Be on Your Radar" but we'd like to take that analysis a little bit further.

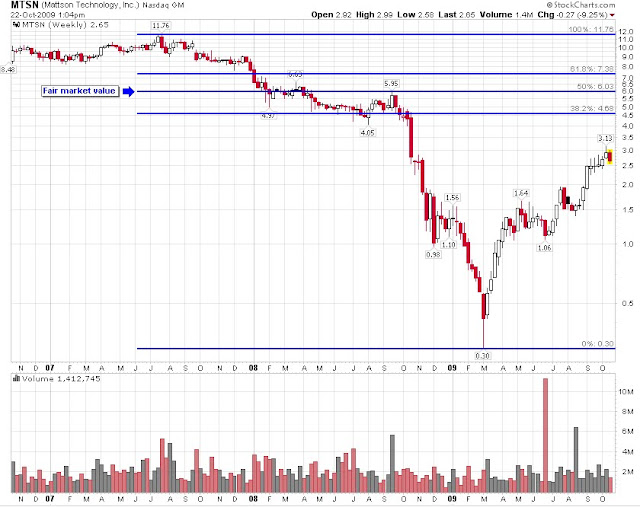

This isn't the first time we've mentioned a company within the chip sector. Our original Speculative Observation on Mattson (MTSN) yielded more than 50% in less than 6 months. Since that write up, MTSN returned 65% while AMAT went nowhere and returned less than 1%.

In pursuit of "seeking fair profits" and being a rather conservative bunch, we had to issue a Sell Recommendation on MTSN at $3.32 on January 6, 2010. Part of our strategy is to constantly search for alternative investment opportunity with a lower risk profile and higher reward potential. With that in mind, you can see that MTSN has outperformed AMAT and the overall market by a wide margin, thus it is fair to say that risk/reward profile is now more favorable for AMAT than MTSN. So let's take a deeper look at AMAT.

Applied Materials (AMAT) is the largest supplier of semiconductor, flat panel display (LCD), and solar equipment according to VLSI Research. The company leveraged their knowledge in LCD market into the solar market in late 2008. There are many growth drivers for this company and the sector. On the chip side, you have China continuing to consume more and more electronics pushing demand for greater chips. LCD driver is coming from conversion from CRT TV to LCD. Solar may get a boost from Obama push for "greener" economy. Though sound bullish in arguments, these factors may already be in the price so we must look at the fundamental.

As of this writing, AMAT is trading roughly around $13.25. This is up considerably (100%+) from AMAT's December 2008 low of $6.24. The company began distributing cash dividends back in 2005 for the amount of $0.09. The current 2010 dividend payout is $0.28 which amounts to a 25% annual increase in dividend. It is expected the that growth rate of the dividend can't be sustain forever but we've taken this is as a positive sign of management's commitment to the shareholders. We at New Low Observer thinks true profits are obtained when a company shows cash rather than paper profits. The current yield of AMAT sits a little above 2% and is quite high on a historical basis. Average yield should be at 1.5%. Take that average yield and you arrive at a share price of $17.35. My proprietary model, which takes into consideration cash flow, earnings, book value, and yield, shows the following price targets:

-

Dirt cheap - $6.75 (we saw AMAT at $6.24 and rocketed up)

-

Buy - $13.26 (we are in that range)

-

Fair - $17.35

-

Over Value - $26.18

*my model changes over time so don't take these prices as static.

For technical analysis on AMAT, please refer back to the article "Applied Material and the Chip Sector Should Be on Your Radar".

So what would we do?

First, we look for other alternatives and stick to our rule of buying low (within 20% of the 52 week low). Because AMAT is 28% above the low, we will not chase it. Alternative investments may be in names like Qualcomm (QCOM) which is 15% above the low. If and when the price retraces on the downside, we'll re-evaluate the situation and may be compelled to buy more.

For anyone who believes that this is an opportunity that can't be missed, I recommend allocating 15% of your portfolio into this name. On top of that, do a two part purchase. First buy 7.5% now and if the shares fall another 20% buy the remaining 7.5% later. This way, the cost basis of the stock would require only a 10% rise to break even. Again, it is not likely that we'll buy AMAT since the alternatives provide exceptional opportunity with less downside risk.

For Research Request of companies on our most recent Watch Lists (only Dividend Achiever or Nasdaq 100), email our team here. We'll post only one research request each week.