Quick Take: U.S. rating downgrade

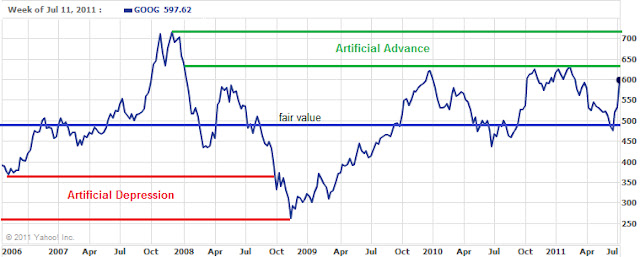

Late Friday evening, Standard & Poor's downgraded the debt of the U.S. from AAA to AA+. The full implications of such action are yet to be known. However, we believe that there are some interesting points to be made. A lower debt rating will require the U.S. government to increase the yield offered on new issuance's. A more competitive yield might draw money out of the stock market and into fixed income securities. As rates rise, utilities and real estate investment trusts (REITs) might come under extreme pressure as the markets try to weight the benefit of holding assets that offer no guarantee and relatively less competitive yields.

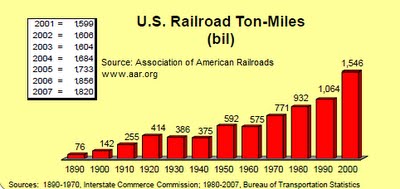

Also, it has not gone unnoticed by us that the U.S. first got tagged with the AAA rating in 1941 and had held that rating through a completed interest rate cycle. It seems almost ironic that the AAA rating ascribed to the U.S. when interest rates were at their lowest would be taken away at the same level 70 years later. We also note that rating agencies tend to show up late to the party. The chart below tells us that it only gets interesting from here.

NLO Dividend Watch List

At the end of the week, our list contained over 120 companies. We had to pare down the number of companies on the list so we decided to post only those stocks trading within 5% of the 52-week low.

| symbol | name | price | p/e | earnings | yield | p/b | % from low |

| GBCI | Glacier Bancorp, Inc. | 12.41 | 21.66 | 0.59 | 3.9 | 1.05 | 0.08% |

| SYBT | S.Y. Bancorp, Inc. | 21.47 | 12.41 | 1.71 | 3 | 1.72 | 0.28% |

| BOH | Bank of Hawaii | 43.04 | 12.77 | 3.37 | 4 | 2.03 | 0.49% |

| O | Realty Income | 30.01 | 28.5 | 1.04 | 5 | 2.21 | 0.81% |

| SFNC | Simmons First National | 23.47 | 11.29 | 2.15 | 3 | 1.03 | 0.95% |

| FNFG | First Niagara Financial | 11.06 | 16.58 | 0.76 | 5 | 0.79 | 1.10% |

| CHFC | Chemical Financial | 18.05 | 13.52 | 1.34 | 4.2 | 0.88 | 1.12% |

| MLM | Martin Marietta | 67.63 | 36.76 | 2.24 | 2 | 2.16 | 1.17% |

| SUSQ | Susquehanna Bancshares | 6.8 | 39.53 | 0.17 | 1 | 0.45 | 1.19% |

| CFR | Cullen/Frost Bankers | 51.28 | 14.53 | 3.5 | 3.4 | 1.46 | 1.24% |

| PRK | Park National | 60 | 13.52 | 4.51 | 5.8 | 1.42 | 1.52% |

| TCB | TCF Financial | 11.83 | 13.77 | 0.99 | 1.5 | 1.07 | 1.55% |

| SON | Sonoco Products | 29.9 | 15.03 | 2.04 | 3.5 | 1.91 | 1.63% |

| CMA | Comerica | 29.13 | 14.98 | 1.68 | 1.2 | 0.88 | 1.75% |

| IBKC | IBERIABANK | 49.18 | 28.84 | 1.84 | 2.3 | 1 | 1.80% |

| ALL | Allstate | 26.29 | 25.06 | 2.45 | 3 | 0.72 | 1.94% |

| EMR | Emerson Electric | 45.39 | 13.99 | 3.11 | 2.5 | 3.15 | 1.95% |

| BRK-A | Berkshire Hathaway | 107k | 16.3 | 6.6k | - | 1.1 | 1.98% |

| MCY | Mercury General | 36.54 | 13.43 | 2.72 | 6.2 | 1.11 | 2.07% |

| MDP | Meredith | 26.56 | 9.56 | 2.85 | 3.4 | 1.58 | 2.08% |

| NTRS | Northern Trust | 41.3 | 16.39 | 2.71 | 2.4 | 1.41 | 2.13% |

| FII | Federated Investors | 19.53 | 12.14 | 1.67 | 4.3 | 3.75 | 2.20% |

| GS | Goldman Sachs | 125.18 | 12.28 | 9.13 | 1 | 0.94 | 2.31% |

| HGIC | Harleysville | 29.5 | 10.56 | 2.79 | 4.7 | 1.03 | 2.36% |

| SEIC | SEI Investments | 17.76 | 14.56 | 1.22 | 1.2 | 3.11 | 2.36% |

| AFL | AFLAC | 41.72 | 10.97 | 4.44 | 2.7 | 1.65 | 2.38% |

| PG | Procter & Gamble | 60.59 | 15.97 | 3.8 | 3.3 | 2.53 | 2.40% |

| BKH | Black Hills | 28.8 | 17.61 | 1.64 | 4.8 | 1 | 2.42% |

| LEG | Leggett & Platt | 19.3 | 16.31 | 1.16 | 4.6 | 1.88 | 2.50% |

| CINF | Cincinnati Financial | 25.97 | 14.36 | 2.27 | 5.8 | 0.84 | 2.53% |

| WMT | Wal-Mart Stores | 50.85 | 11.11 | 4.58 | 2.7 | 2.68 | 2.54% |

| AVY | Avery Dennison | 29.12 | 10.47 | 2.88 | 3.2 | 1.72 | 2.57% |

| UBSI | United Bankshares, Inc. | 22.66 | 13.73 | 1.66 | 4.8 | 1.24 | 2.58% |

| ANAT | American Nat'l Insurance | 76.02 | 12.85 | 5.91 | 4.1 | 0.55 | 2.59% |

| WEYS | Weyco Group, Inc. | 22.83 | 19.85 | 1.15 | 2.5 | 1.48 | 2.61% |

| NWN | Northwest Natural Gas | 42.8 | 16.31 | 2.62 | 3.7 | 1.58 | 2.64% |

| AVP | Avon Products | 23.21 | 13.56 | 1.62 | 3.3 | 4.87 | 2.72% |

| TDS | TDS | 25.47 | 19.59 | 1.3 | 1.6 | 0.7 | 2.83% |

| RBCAA | Republic Bancorp | 17.29 | 3.95 | 4.36 | 2.9 | 0.83 | 2.86% |

| CYN | City National | 48.58 | 16.09 | 3.02 | 1.5 | 1.27 | 2.95% |

| BXS | BancorpSouth | 11.92 | 25.36 | 0.16 | 0.3 | 0.83 | 3.03% |

| LLTC | Linear Technology | 27.08 | 10.83 | 2.36 | 3.1 | 12.52 | 3.08% |

| MRK | Merck & Company | 31.71 | 59.94 | 0.53 | 4.2 | 1.79 | 3.12% |

| EV | Eaton Vance | 23.29 | 15.12 | 1.54 | 2.5 | 5.71 | 3.14% |

| TRH | Transatlantic Holdings | 45.24 | 17.2 | 3.06 | 1.7 | 0.69 | 3.17% |

| TEG | Integrys Energy Group | 47.58 | 12.67 | 3.75 | 5.2 | 1.23 | 3.19% |

| NUE | Nucor | 34.95 | 23.6 | 0.82 | 3.6 | 1.48 | 3.22% |

| SCG | SCANA Corp | 37.32 | 12.56 | 2.97 | 4.7 | 1.24 | 3.38% |

| VLY | Valley National Bancorp | 12.15 | 14.45 | 0.77 | 5 | 1.6 | 3.47% |

| VNO | Vornado Realty Trust | 80.78 | 18.75 | 4.31 | 2.8 | 2.61 | 3.48% |

| ADM | Archer-Daniels-Midland | 28.64 | 9.15 | 3.25 | 2.1 | 0.97 | 3.58% |

| FCBC | First Community Banc | 12.04 | 9.48 | 1.25 | 2.7 | 0.76 | 3.70% |

| ECL | Ecolab Inc. | 47.78 | 21.51 | 2.23 | 1.4 | 4.77 | 3.71% |

| UVV | Universal | 36.33 | 6.7 | 5.42 | 5.1 | 0.84 | 3.74% |

| VAL | Valspar | 30.17 | 13.94 | 2.16 | 2.1 | 1.82 | 3.78% |

| BMI | Badger Meter | 35.27 | 20.04 | 1.76 | 1.5 | 3.01 | 3.80% |

| GCI | Gannett Co. | 10.8 | 5.07 | 2.13 | 2.3 | 1.19 | 3.85% |

| LOW | Lowe's | 20.15 | 14.18 | 1.42 | 2.4 | 1.53 | 4.13% |

| PEP | Pepsico | 64.67 | 16.45 | 3.74 | 3.1 | 4.17 | 4.22% |

| SJW | SJW | 22.86 | 17.2 | 1.28 | 2.8 | 1.67 | 4.48% |

| MUR | Murphy Oil | 55.2 | 11.64 | 4.74 | 1.6 | 1.29 | 4.55% |

| FFIN | First Financial | 30.44 | 14.79 | 1.99 | 2.8 | 2 | 4.85% |

| KMB | Kimberly-Clark | 64.07 | 15.12 | 4.4 | 4.1 | 4.22 | 4.93% |

Top 5 Performance review

In our ongoing review of the NLO Dividend Watch List, we have taken the top five stocks on our list from August 6, 2010 and have check their performance one year later. The top five companies on that list can be seen in the table below.

| Symbol | Company | 2010 | 2011 | % change |

| PBI | Pitney Bowes Inc | 20.71 | 20.02 | -3.33% |

| WST | West Pharmaceutical Services | 35.26 | 41.91 | 18.86% |

| PAYX | Paychex, Inc. | 25.56 | 27.09 | 5.99% |

| HGIC | Harleysville Group | 30.9 | 29.5 | -4.53% |

| CWT | California Water Service Group | 17.49 | 18.09 | 3.43% |

| Average | 4.08% | |||

| ^DJI | Dow Industrials | 10653.56 | 11444.61 | 7.43% |

| ^GSPC | S&P 500 | 1121.64 | 1199.39 | 6.93% |

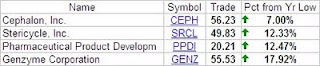

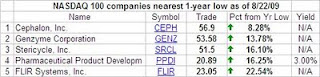

The top 5 companies on our list last year underperformed the major indexes by a wide margin. However, in the chart below, you'll notice that all 5 stocks achieved 10% gains (our ideal target for selling) within 4 months of the August 6th posting; such a gain approximates nearly 30% annualized returns. We cannot emphasis enough the value of selling these stocks if a 10% gain is accomplished within a year while inside of a tax-deferred account. As you can see, the year end results vastly differ from the gains that could have been made.

Please consider donating to the New Low Observer. Thank you.