On October 12, 2022, Chevron CEO Mike Wirth was featured in a Financial Times article titled “Chevron Chief Blames Western Governments for Energy Crunch.” In this piece, we attempt to deconstruct the many ways that the claims by Wirth are inaccurate.

To embark on a discussion of this nature, it is important to understand our take on the topic of oil companies and the government’s role in economic affairs.

In the past, we have bought and sold energy companies as part of our investment portfolios. Our track record has been a mixed bag of modest successes and failures. In terms of our macro analysis, we’ve had more luck in analyzing market trends. One aspect that we’ve been consistent with is a non-narrative approach to the energy sector. This means that we do not emphasize the glowing prospects or the dire nature of the industry. Instead, we focus on the price action and the historical precedent and not much else.

As outlined in many twitter postings, we are for as little government involvement as possible. We believe that price will, as it always has, dictate the needed direction for markets. However, we’re cognizant of the fact that “government happens” and therefore are accepting of the role that government plays on many economic issues.

Anyone who has stumbled across our twitter feed @NewLowObserver in the last two years will notice that our strongest claims are against government involvement with markets and that solid economic analysis and conclusions begins with data from exceptional precedent. With this in mind, we will go back in time to help draw upon what we believe is a more accurate view of the government and oil industry’s role in the current environment.

Our Thoughts on the Oil Sector

It has been our contention that if you want to know all about a business or industry, you only need to look at the stock index or the stock price and you can infer enough to make some reasonable assumptions for now and the not too distant future. In the following examples, we highlight what we’d like to always accomplish when assessing markets. Basically, these are exceptions but they are what we strive for when examining any industry or market.

2012: Chesapeake Energy

We didn’t know much about Chesapeake Energy other than they were in the shale fracking business and the CEO was very popular in the industry. On April 26, 2012, we wrote a short piece on Chesapeake Energy outlining the prospects.

We opened with the line, “While it appears that Chesapeake Energy (CHK) has seen all the punishment that could possibly lay ahead, we’re concerned that the previous technical pattern in the period from 1993 to 1999 is about to repeat” and warned that “If CHK falls significantly below the $4.94 level, then the stock has a high likelihood of going all the way $0.67.”

What you should notice is that we did not talk about industry trends, emerging headwinds, possible decline in earnings, proven/probable reserves, life of wells, age of rigs, etc. We only focused on the stock price. Chesapeake filed bankruptcy in 2020.

2015: NYSE Arca Oil and Gas Stock Index

In September 7, 2015, we reviewed the price structure of the NYSE Arca Oil and Gas Stock Index and concluded “...we hazard to guess what would happen globally to the oil market in order to decline to such a low point.”

Again, we didn’t assess the market based on the political climate, global warming regulations, growth/decline of global demand. Instead, we simply looked at the price and gave our opinion. In March 2020, the price of oil dropped to negative levels in the near term contracts.

2020: SPDR S&P Oil & Gas Exploration & Production ETF

Finally, in April 2020, we highlighted the need to consider $XOP after it was clear that that prices in the oil sector had gone too low.

The point of the historical look at our work is to emphasize that our goal is price and not narrative. We don’t care about the political arguments of either side of the aisle as they don’t rely on evidence that can be substantiated. This absence of evidence then relies heavily on narrative which, if well crafted, can be effectively used regardless of the reality.

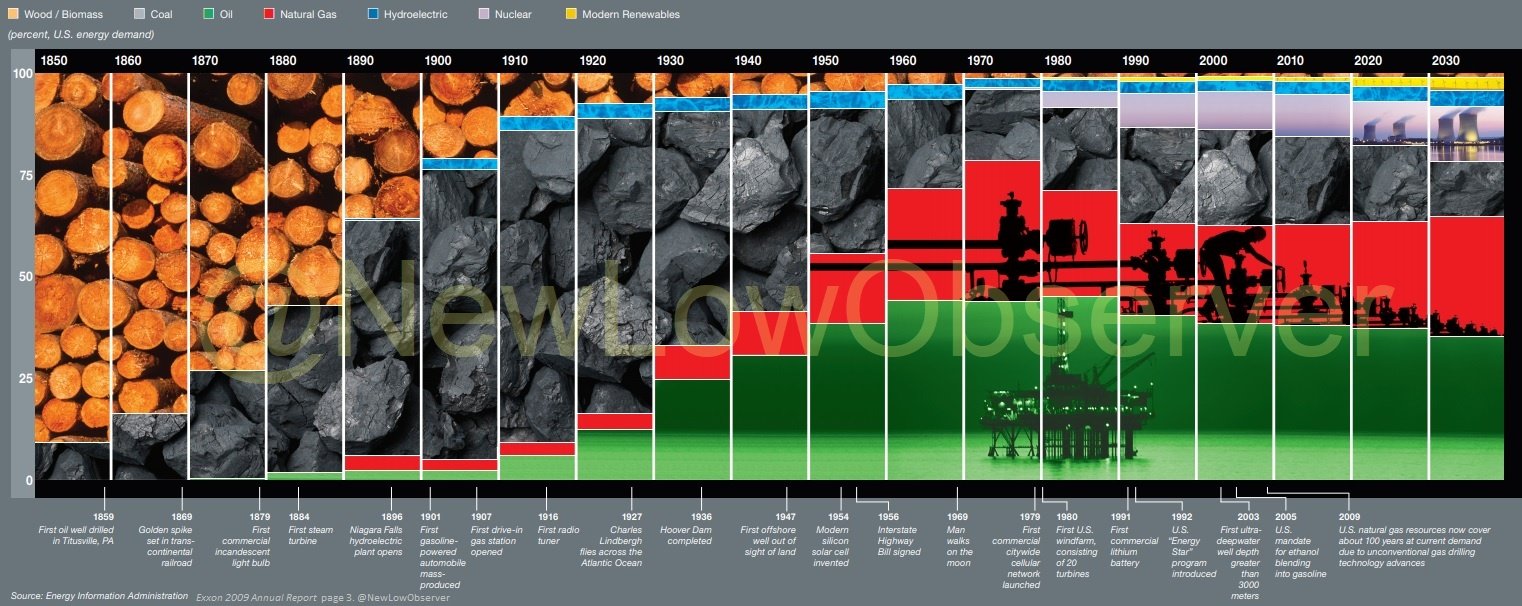

In this vein, we have hammered away at the narrative of those who claim oil is running out and therefore we are obligated to craft policies that don't consider the frictional costs for bridges to nowhere. With this in mind, we hope you’ll indulge us with a rebuttal to the remarks made by Mr. Wirth.

“Western Governments Have Made a Global Oil and Gas Crunch Worse”

“Western governments have made a global oil and gas crunch worse by ‘doubling down’ on climate policies that will make energy markets “more volatile, more unpredictable, more chaotic”, the head of US supermajor Chevron has warned.”

There are several narratives based on the above claims that require full examination in this critical opening paragraph. Without going too far back in time, we shall demonstrate how the opposite of Mr. Wirth’s claim is the reality.

If we look at the trajectory of oil prices since the 2008 peak, the trend has been down.

Most notable in the decline of the price of oil is the price of almost every other commodity from 2011 as highlighted in the Invesco DB Commodity Index Tracking Fund.

If the claim is that oil is the largest component of the commodity index then look at the 2011 peaks experienced by gold, silver, copper, platinum, natural gas, heating oil, corn, soybean oil, cotton #2, orange juice, etc.

If climate policies favoring alternative energy pushed down the use, consumption, or investment in fossil fuels then why is the laundry list of other commodities struggling under the same weight of the 2011 peak?

Let’s invert the question and ask, is it possible that government’s “doubling down” in support of the oil industry caused the price of oil to go negative in 2020? How could this be?

From 2016 to 2018, Federal land sales for drilling oil and gas increased at an exceptional rate while the overall trend of all commodities was in decline, a mistake that pushed the industry to glut conditions. Can we not say that government has been very supportive of the oil & gas industry and the consequences of such support has actually been more disastrous than the push for the “renewables.” [Don’t get us started on renewables]

We couldn’t help but notice that Chevron is experiencing a surge in the stock price to new highs after getting through oil prices going negative, presumably due to the government’s eager intervention that helped defy the declining trend of the market from 2011.

From the price history, the trajectory of Chevron shares seem to be a continuation of a trend that has been in place since the 1974 lows. It appears that the bonuses that will be given out to Wirth in the coming year will be well earned. However, we cannot accept the claim that Chevron has suffered at the hands of the government when the market says everything appears on a trend that has been in place since 1974, a period when government policy has strongly favored the oil industry.

see also: